There has been speculation in recent weeks that the Federal Reserve may pause in its interest rate increases. Fed Chairman Jerome Powell said recently that interest rates are just below their normal levels, which many took to be a signal that we may be nearing the end of the interest rate hiking cycle that began in 2015. The stock market seemed to think that was what he meant as it went on a tear in the days following the announcement, reversing several weeks of steep declines, before falling sharply once again.

The market initially reacted so positively to Powell’s remarks in part because his comments seemed to show some awareness of the Fed’s record of success in managing the economy during periods when it is increasing interest rates. It isn’t good.

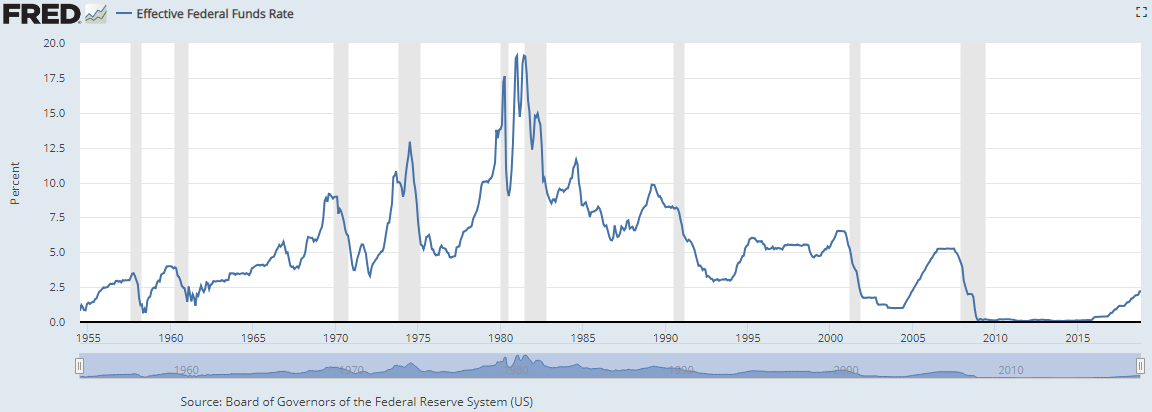

The chart above shows that the Fed appears to have a history of over-tightening when it comes to interest rate hikes. The blue line represents the Federal Funds rate set by the Fed while the shaded bars represent recessions. The thirteen periods of Fed tightening have ended in recessions ten times, which is not a great batting average for managing the economy. The argument against the Fed is that it pushes interest rates up too high, hamstringing the economy and forcing it into recession.

That conclusion may be a bit too simple to fit the overall reality, however. As with many things in life, trying to find the one magic factor that controls something as complex as the U.S. economy is far too simple. Each of our recessions has been a unique event with multiple causes.

We need only look at the two most recent slowdowns to illustrate this. The Fed did raise interest rates from June 2004 through August 2006, but that was not the cause of the 2008 recession, which was driven largely by the subprime mortgage crisis and the near failure of the entire financial system. The 2001 recession occurred largely as the result of the bursting of the dot-com bubble, a drop in business investment after heavy spending in 2000 and the September 11th attacks – events unrelated to the Fed hiking interest rates from July 1999 through July 2001.

This doesn’t let the Fed off the hook. With the benefit of hindsight, many economists have noted that while the Fed did not directly cause the recessions by hiking interest rates, it raised rates too high and hampered the recovery.

In any event, the Fed would be wise to pause in its interest rate hikes to assess how the economy is functioning on a variety of levels and whether if it is handling the increase in rates. With the current Fed Funds rate at 2.25%, the Fed has finally reached the point where it has some wiggle room if it needs to lower interest rates to help stimulate the economy if it runs into trouble. Economists we speak with do not foresee a recession in 2019, but that is just the problem with recessions: no one ever sees them coming.

Social Media