As stocks rose strongly to finish out 2016 and with the Fed poised to increase interest rates, I have had several clients ask why we are still holding bonds. The obvious reason, of course, is income. Bonds pay regular interest and, if you are retired or rely on your portfolio for your income needs, bonds are an important source of funds that allow you to take money out of the portfolio without reducing your principle. There is another, equally important, reason, however.

If you’re a regular reader of our quarter-end and mid-quarter market commentaries I’m sure you already know that reason. Bonds act as ballast in your portfolio during rocky times. Obviously, this can hold back returns somewhat when stock prices are surging higher, but when stocks are plunging and fear is high, bonds help cushion the sharp losses you would otherwise suffer.

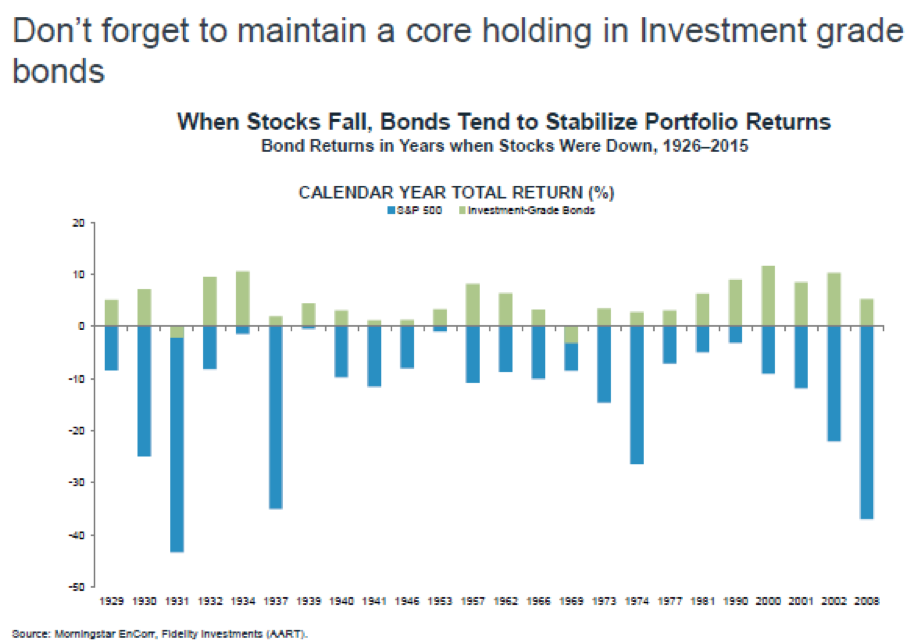

I recently came across a chart from Fidelity that shows at a glance why bonds are a vital part of a properly constructed investment portfolio. The chart shows the performance of high-quality investment-grade bonds in the years that stocks were down from 1926 through 2015. Out of the 24 years of stock losses, bonds rose in every year except for 1931 and 1969 and those two losses were much less than the losses in stocks.

Limiting losses can be as important as participating fully in gains over the long term. For example, if you bought Stock A for $100 and it dropped 10% to $90 in the first month then gained back 10% the following month, that stock would be worth only $99. If you bought Stock B that only fell 5% in the first month to $95, but then gained only 5% in the second month when Stock A rallied much more strongly, your stock would be worth $99.75, which is more than Stock A even though it only had half of Stock A’s second month gains. Limiting losses on the way down gives you a much smaller hurdle to clear on the way back up.

Investment grade bonds are much less volatile than stocks and provide that loss-limiting cushion that helps make long-term gains easier to achieve. You can see just how less volatile bonds are by looking at annual returns for stocks and bonds over time. Since 1980, the Barclays Aggregate Bond Index’s worst year was 1994 when it declined 2.9%. The worst year for stocks was 2008 when the S&P 500 plunged 37.0%. That year, the Barclay’s Aggregate Bond Index rose 5.2%. That was not enough to offset the steep stock losses, but investors who had investment grade bonds in their portfolios lost significantly less than those who were all in stocks because they worried about beating the stock market on the way up.

It is often said that a bad day for stocks is usually much worse than a bad year for bonds. With the stock market at record highs, it is tempting to jump on the bandwagon and neglect fixed income, but it is very difficult to predict market corrections and car accidents. It’s always a good idea to have insurance.

Social Media