On September 18, 2024, the Federal Reserve cut interest rates by 0.5% (50 bps), marking its first rate cut since the early days of the COVID pandemic in 2020. This change in interest rate policy presents a good opportunity to examine the advantages and disadvantages of owning different types of fixed-income investments during periods of rate cuts.

Money market funds have been an attractive holding since the Fed began aggressively raising interest rates in its battle against inflation. These funds not only offered a higher yield but also maintained their value, while traditional bond mutual funds lost ground as money flowed into shorter-term investments. When interest rate decline, however, money market funds become less attractive than holding core bond funds.

Money market funds hold short-term, highly liquid debt instruments and pay interest based on prevailing short-term rates. When the Fed cuts rates, money market yields immediately decline, yet there is no gain in price since money market funds are always valued at $1. Traditional bond funds hold longer term government, agency and corporate bonds and outperform money market funds during periods of falling rates because the value of the bonds they own rise when interest rates decline. In a simple example of why that happens, suppose you own a ten-year bond paying a 5% coupon. If interest rates fall and newly-issued bonds now pay only 4%, your bond that pays a higher coupon over a longer period of time is more attractive and people are willing to pay you more for it.

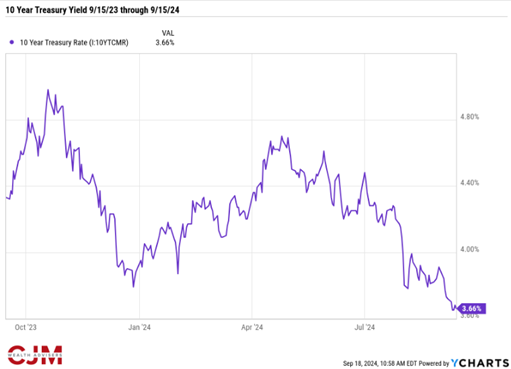

This declining yield scenario is what has paid off for bond funds over the past year. The yield on the 10-year Treasury bond has followed a rocky path, but as shown in the chart below, the recent yield (as of 9/15/24) of 3.66% is lower than the yield of 4.33% a year earlier.

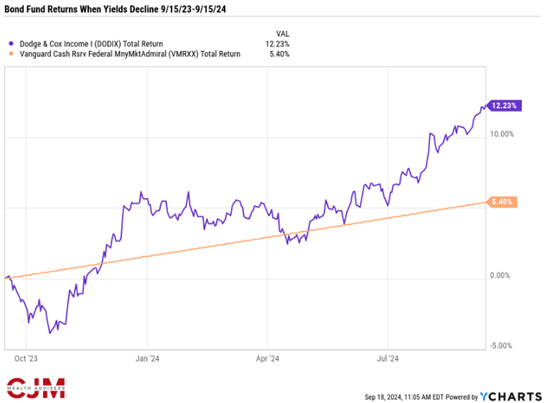

This 67 basis point (0.67%) decline in yield had an outsized impact on the relative performance of longer-term bonds funds, such as the Dodge & Cox Income Fund (DODIX) – a top-performing core bond fund that we use in many client portfolios. For the one-year period, Dodge & Cox has performed especially well compared to money market funds, such as the Vanguard Cash Reserve Federal Money Market Fund (VMRXX). As shown in the chart below Dodge & Cox surged 12.23% over the one-year period, while the money market fund gained less than half of that (5.40%).

Since money market funds neither increase nor decrease in value, the only return investors enjoy is the yield on the fund – the 5.40% shown in the chart above. That yield is tied to the Federal Reserve’s federal funds rate. With the Fed now cutting that rate, money market yields will decline, making them less attractive going forward.

Traditional bond funds provide yield, of course, but they have an additional source of returns that money market funds do not: capital appreciation during periods of declining interest rates. Dodge & Cox Income Fund’s yield and the capital appreciation on its underlying bonds combined to make up its 12.23% return in the chart above.

There are still cases where money market funds may be preferred. If you need a short-term place to park cash, money market funds remain a solid option. However, for longer-term investment, longer-term bond funds are often a better option when rates are declining. They can improve returns and provide income while still offering protection against stock market volatility.

The above does not constitute investment advice, and past performance is not an indication of future future results. Every client’s situation and risk tolerance is different.

Social Media